Project Information

- Category: Software

- Client: PhD Student

- Project Date: 19 Oct, 2024 - 13 May, 2025

- Project Source Code URL: View on Github

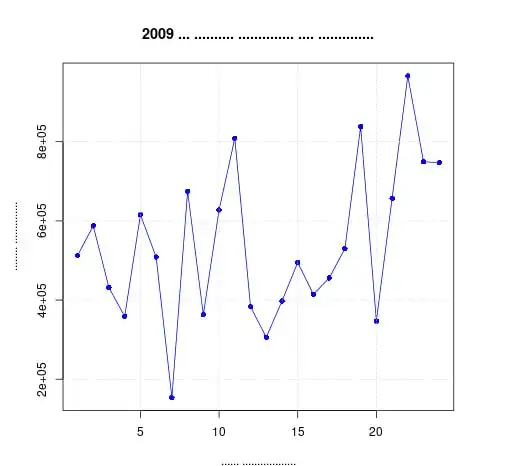

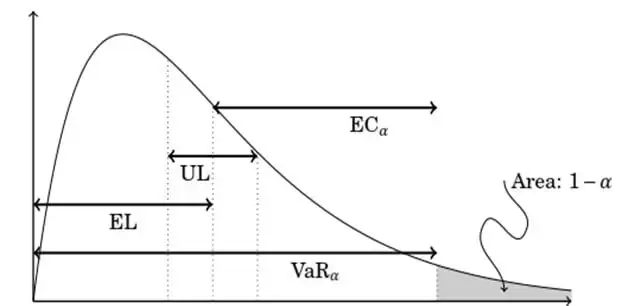

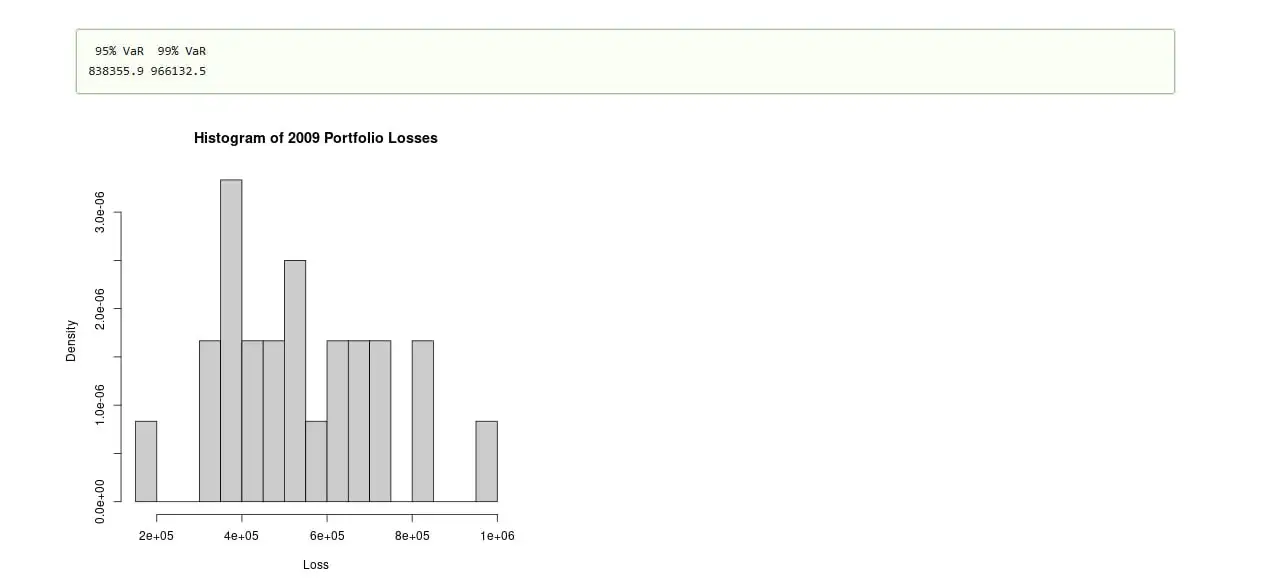

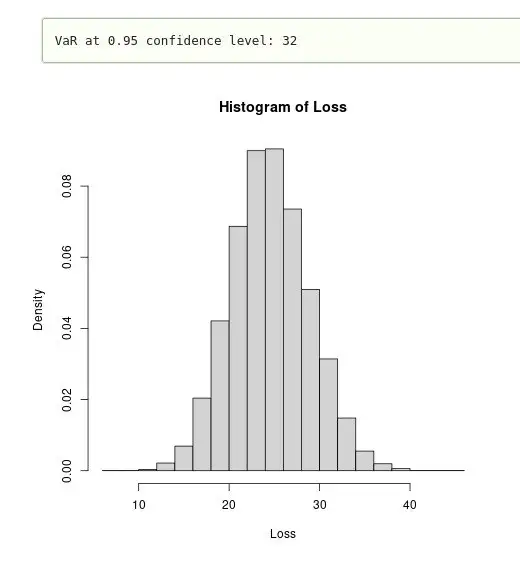

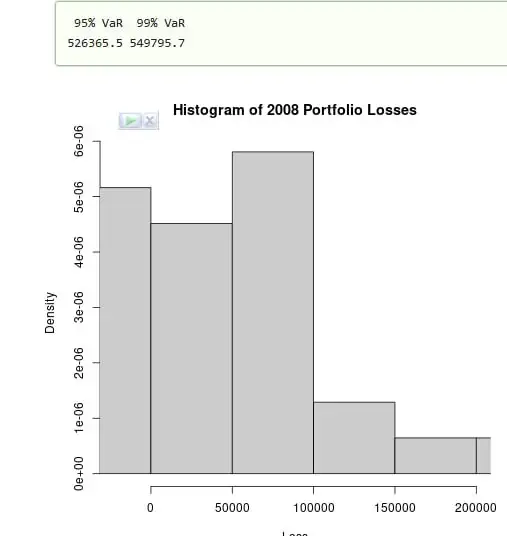

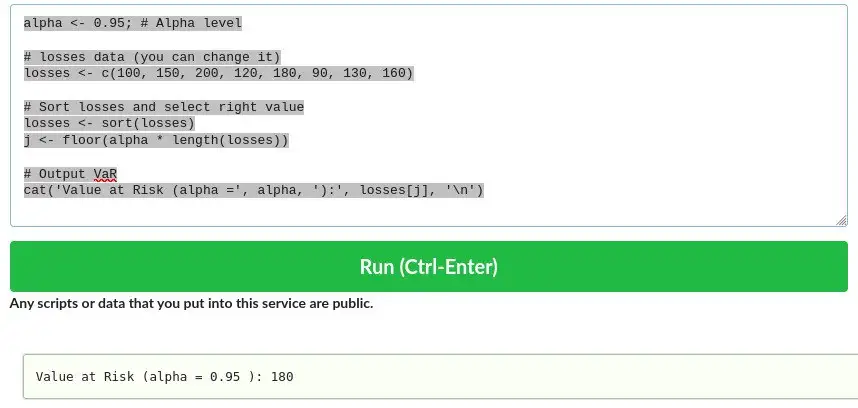

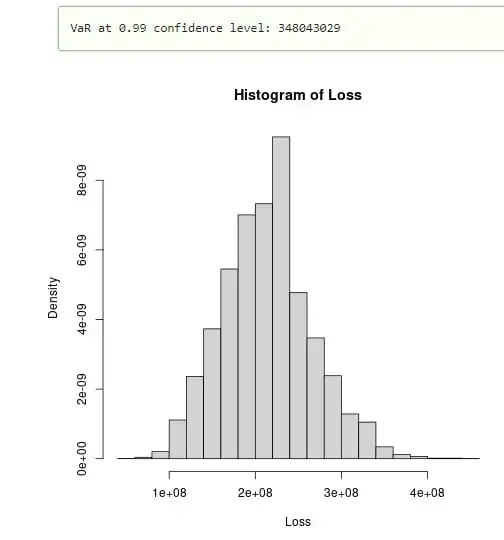

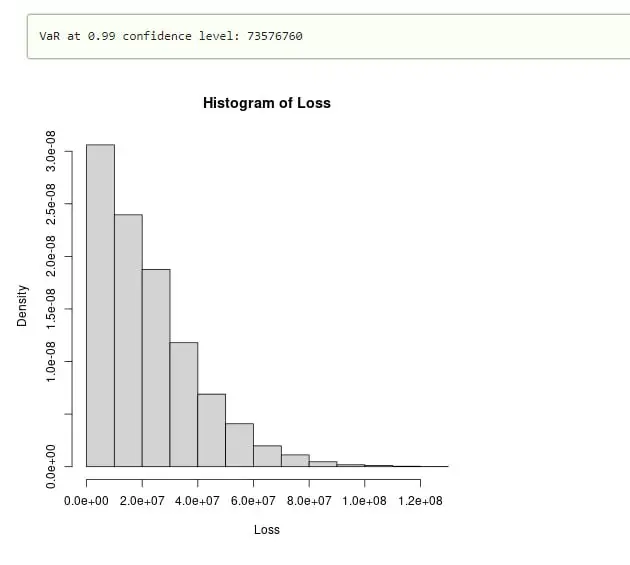

Credit Portfolio VaR Simulation Using Monte Carlo in R

Developed a Monte Carlo credit-loss engine in R using PD/LGD/EAD inputs, simulated portfolio loss distributions, and estimated VaR (e.g., 95% / 99%) to quantify tail risk and support credit risk decision-making.